By Andrew Royal, Head of APAC Autobahn Analytics and Algorithms, Deutsche Bank

In general, there is a tradeoff that needs to be made: Price impact can occur when participation rate is too high, and as a result cost may increase for a given volume. Even if we attain the close price exactly, there is still a market impact due to the existence of our volume – the price could have been more favorable. The alternative is to start trading early with a lower participation rate, but this exposes the trader to price and time risk.

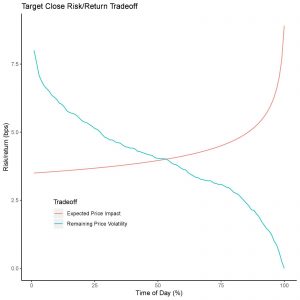

The price risk/expected impact tradeoffs can be graphed in an idealised setting. Impact will increase as we get closer to the end time and participation rate starts increasing rapidly – this is the red line in figure 1. Conversely, price risk declines as we get closer to the end time – this is the green line in figure 1:

In markets that are liquid and have a close auction mechanism, executing all volume during this session is more likely if your order is not a large proportion of the close. For example, Australia close auctions generally trade around 22% of the full day volume (source; Deutsche Bank, February 2019) – small orders of less than 5% ADV will tend to get fully executed during this session with little to no price impact. From a modelling perspective, the more interesting problems come about from large orders that are expected to create some degree of price impact.

Intuitively, therefore, we have two main cases:

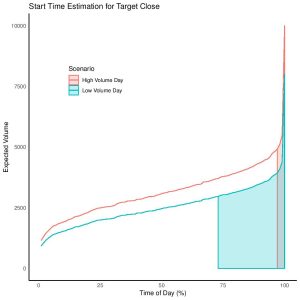

– High expected market volume is the easy case; we don’t expect much market impact and the best is to start as late in the day as possible in order to get as close to the close price benchmark.

– Low expected market volume implies high order participation rates for a given order size. To avoid the impact from high order participation rates, we must start earlier in the day but the trade off is we incur extra price risk.

The risk appetite of the client will determine how much price risk they value per unit of price impact. The sum of both risks gives us a minimal total risk – this allows us to calculate an optimal start time.

When volumes spike up, market impact tends to decline purely as a result of lower expected participation rate. In figure 1, this pushes the start time closer to the end of day for a given price volatility profile. What the client will actually see is not the tradeoffs that the strategy is making behind the scenes, but the following what is shown in figure 2.

Estimating future volume

As a result of the optimal trade off considerations, good stock volume and price volatility predictors are very important if we want to reduce impact in a consistent way. In what follows we shall focus only on the stock volume prediction problem.

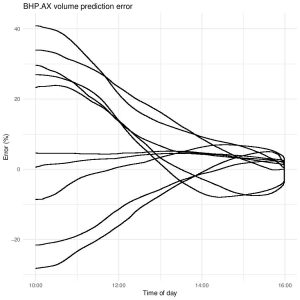

Some examples of how a volume predictor calculates the full day volume are shown in figure 3.

Some examples of how a volume predictor calculates the full day volume are shown in figure 3.

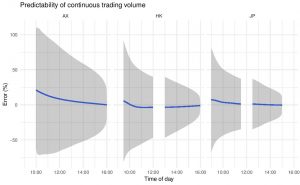

A volume predictor using Bayesian inference can be used to incorporate new data as it arrives throughout the day. As expected, we reduce forecast error over the course of the day.

We can aggregate all of these sample paths to give a view of how the average stock will perform as in figure 4. The blue line in the plot below shows mean-bias (zero is perfect estimate), while the grey zone indicates standard deviation around the mean bias line. As one expects, the grey uncertainty zone narrows as more information is incorporated into the volume predictor and gives us better estimates. By midday we have eliminated much of the uncertainty, and we can then use this information as input into start time algorithm.

We can aggregate all of these sample paths to give a view of how the average stock will perform as in figure 4. The blue line in the plot below shows mean-bias (zero is perfect estimate), while the grey zone indicates standard deviation around the mean bias line. As one expects, the grey uncertainty zone narrows as more information is incorporated into the volume predictor and gives us better estimates. By midday we have eliminated much of the uncertainty, and we can then use this information as input into start time algorithm.

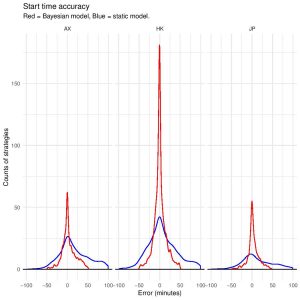

Optimal start times can be inferred for a 10% ADV order running at an expected 10% participation across each region. Generally, the start time is unbiased, but the accuracy as measured by the standard deviation declines dramatically by choosing the Bayesian volume predictor as shown in figure 5. Here, a positive error means we start after the optimal time – we will incur greater expected price impact as a result of running at a higher participation rate than expected.

Optimal start times can be inferred for a 10% ADV order running at an expected 10% participation across each region. Generally, the start time is unbiased, but the accuracy as measured by the standard deviation declines dramatically by choosing the Bayesian volume predictor as shown in figure 5. Here, a positive error means we start after the optimal time – we will incur greater expected price impact as a result of running at a higher participation rate than expected.

Conclusion

The target-close algorithm is a necessary tool to better manage large ADV orders with a close price benchmark. A properly constructed target-close model allows traders to mitigate their market impact by balancing it off against price risk.

This article describes market specific modelling techniques used at Deutsche Bank that are aimed at striking this balance that reduces the price impact of large orders with a close benchmark. Deutsche Bank is continually evolving its execution algorithms with a focus on building data driven improvements into the product. Target Close is available in all Autobahn 2.0 markets in APAC.