This is the fourth installment of a content series sponsored by CODA Markets

When I left the world of high-speed market-making back in 2014, friends were flummoxed. Auctions? Really? Nice for openings, nice for closings, but all-day long? What are you thinking?

Auctions are not new, obviously. The New York Stock Exchange ran them from 1812 to 1870, only conceding the future to continuous trading when the existing floor technology could no longer keep pace with the growth in public listings and trading demand. Today, of course, we can do auctions electronically. More than a third of NYSE volume in NYSE-listed shares is done in their opening and closing auctions.

But why stop there? Why not do them all day long—on-demand, whenever traders want them? Well, here are the reasons I still hear:

You can’t trade more than 150 shares of anything without tipping your hand. This is true—in a continuous market with bilateral transactions. But in an auction, you can trade tens of thousands of shares without moving the market. Why? Because you don’t have to identify yourself or how many shares you want to trade—or even whether you want to buy or sell.

In a CODA auction, all you have to tell the world is that you (anonymously) want to trade a given stock. Then you sit back—between 5 milliseconds and 30 seconds, depending on your preference—and watch the counterparties come to you. If you don’t trade, no one’s the wiser. If you do trade, whether against one counterparty or ten, 500 shares or 50,000, the multilateral transaction that prints tells the world nothing about where the market is headed. Did a buyer initiate? A seller? No one knows—so future prices don’t budge.

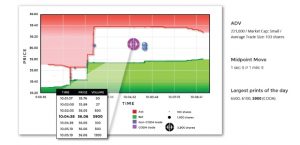

Consider this trade in Pfizer stock, in which a $3M+ transaction had just printed one tick outside of a thin NBBO. CODA’s multilateral auction facility allowed a liquidity seeker to offer down an extra penny on the $40 stock, and to capture 50 times the lit bid size—all with virtually no impact.

Pfizer, Inc. “PFE” – October 23, 2018

Ok, but liquidity is good enough in the continuous markets. Good enough? If you can trade 50,000 shares in one go, simultaneously against multiple counterparties, without revealing who you are or whether you are buying or selling, the market impact should still be less than trading 150 shares bilaterally, sequentially, 333 times, particularly when the market can infer whether a buyer or a seller is moving it. And when the stock is thinly traded, auctions really show their worth in aggregating liquidity and minimizing signaling.

Consider this trade in Assembly Biosciences. In the five minutes before the CODA auction, a total of 6,000 shares changed hands, pushing the thinly traded stock up from $35.35 to 36.05. The CODA Block 30-second auction aggregated diverse liquidity, resulting in a single print of 5,900 shares—without moving the price. Again, CODA’s symbol-only alerts minimized market impact.

Assembly Biosciences, Inc. “ASMB” – October 3, 2018

Ok, but the NBBO on thinly traded stocks bounces all over the place, and auctions can’t do anything to help with that. Not so. If you know the price at which you’d happily trade your block, inside or outside the NBBO, initiate an auction! You have nothing to lose but your fear of leakage. You may get some or all of your order done, at that price or better. And if you don’t—try, try again (or let your algo do it). No one will know what you’re up to.

Consider this trade in Beazer Homes, where two earlier auction attempts shot blanks. Just one minute after the second auction finished, a separate natural initiated an auction of their own, and the alert brought the original order back in for a complete fill. The lesson is clear: your first try may not bring joy, but so what? CODA Block has a daily unique symbol hit rate of 33%—so give it another shot a bit later. Or try a more aggressive price. Victory goes to the persistent and the bold.

Beazer Homes USA “BZH” – October 2, 2018

Ok, but you cherry-picked your great trades. Not so. Consider this recent study by ViableMkts, their “CODA Block Execution Quality Report”: http://www.pdqenterprises.com/wp-content/uploads/2019/01/ViableMkts-CODABlockAnalysis-12-Month-final.pdf. ViableMkts independently examined twelve months of CODA Block trades, and their numbers back me up. The study concluded that initiating CODA auctions offered “a valuable tool for trading institutional size with little downside and potentially large benefits.”

Ok, so on-demand auctions are great, but I can’t afford to ignore good prices when I see them. Not to worry. Algorithmic solutions are available from your broker, or from CODA directly, that seamlessly integrate on-demand auctions with access to the continuous markets. You don’t have to give up the old to partake in the benefits of the new.