David Howson, president of Cboe Europe, said Periodic Auctions and Large In Scale volumes will continue to grow and the exchange is exploring offering new order types to further enhance liquidity.

Howson took on his current role at the start of this year from Mark Hemsley, who retired from the company. He had previously been chief operating officer of Cboe Europe since 2013.

He told Markets Media that Cboe Europe expects continued growth in Periodic Auctions and LIS as existing clients are looking for ways to extend their interactions with these platforms and there is a healthy pipeline of new clients onboarding to use these services.

“We are exploring offering new order types to further enhance the liquidity on our market,” Howson added. “For block trades we are enhancing the workflow to increase matching.”

In addition Cboe Europe launched a closing cross mechanism, 3C, last year which he said is being used more actively. “We have seen good flow in Europe and there is a decent pipeline so we expect volume will continue to grow over the coming months,” he said.

3C is a post-close trading service for customers looking to execute across the 18 European markets that the exchange serves as increased volumes are being executed in the closing auction and post-close trading session in Europe. In addition, many exchanges charge higher fees during this period.

The mechanism is independent from the listing exchange and does not depend on their closing auction price. It uses an “at limit” order type, so orders can only be entered and matched at the participant’s specified price. Market participants are able to see the price and size/quantity for all levels predicted to execute in the cross in real-time.

The increase volatility as a result of the Covid-19 pandemic led to a rise in across all exchanges. Howson noted there have been no problems in trading or clearing despite all staff working from home on some of the exchange’s heaviest volume days.

“On February 28, overall market volumes reached over €100bn ($108bn), the largest volume day since the referendum on the UK leaving the European Union,” he added. “We have also seen volume records in our Periodic Auctions Book and Cboe LIS.”

Cboe reported in its results for the first quarter of this year that net revenue for European equities increased by 15% from a year ago to $26.2m.

Cboe Global Markets Reports Record Results for First Quarter 2020. See the press release: https://t.co/DBFCQJ5Sd0. pic.twitter.com/Hgcq07TZat

— Cboe (@CBOE) May 1, 2020

The exchange said Cboe European equities had 17.7% market share in the first quarter of this year, down from 22.1% in the first quarter of 2019, which was primarily as a result of significant market profile shifts. Highly volatile market conditions during the quarter saw some participants recalibrate their models or retrench from the market.

“In the first half of March some funds managers were looking for actionable liquidity and recalibrating their models and volumes rose on the lit central limit order book,” said Howson. “Spreads widened about five to six times the average, but fell back to between two to three times average in early April.”

Launch of European equity derivatives exchange

Howson confirmed that the exchange is still planning to launch Cboe Europe Derivatives, a new exchange, in the first half of next year. “The Covid-19 pandemic may lead to some short-term bumps in the road, but it does not alter our long-term plan or strategy,” he added.

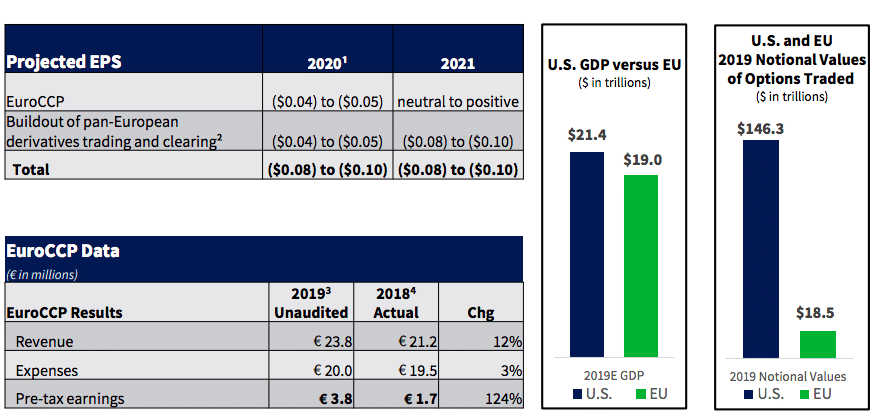

In order to launch the new exchange, Cboe announced the acquisition of EuroCCP, the pan-European equities clearing house in December last year. EuroCCP clears trades for 39 trading venues, which represent close to 95% of Europe’s equity landscape.

Ed Tilly, president and chief executive of Cboe Global Markets, said on the first quarter results call that the exchange will look to provide an alternative market model and introduce efficiencies available in the US market .

He continued that Cboe expects to offer exposure that represents multiple European markets through index futures and options, single-name futures and options and other products.

MiFID II review

Last month the European Securities and Markets Authority published responses on its review of certain aspects of MiFID II as the regulator had wanted to the EU regulation to increase trading on lit venues in the region, which has not happened.

📢ESMA has published responses to the consultation on MiFID II MiFIR review – equity transparency, DVC and trading obligation.

— ESMA – EU Securities Markets Regulator 🇪🇺 (@ESMAComms) April 23, 2020

🔗 https://t.co/PBNEKlDkXV pic.twitter.com/Cy9xdJx5jV

Howson said: “Buy-side participants find utility in access to a range of execution mechanisms so they can optimise performance for their strategies. If the number of execution mechanisms is constrained through an artificial quota they cannot meet their best execution requirements.”

In their responses fund managers also argued that systematic internalisers, dark venues and periodic auctions have saved money for end-investors and there are other ways to increase transparency, such as introducing a consolidated tape. The sell side responses also said that forcing trades onto lit venues will harm best execution and want the share trading obligation and double volume caps removed from MiFID II.

Howson wrote a letter to clients on the consultation and the exchange’s response. He said: “Many of the areas consulted on need careful consideration in order to avoid causing damage to European equity market structure and we have provided a robust response.”

The response said there is no fundamental issue with the balance of trading between available trading mechanisms.

“This becomes apparent when activity that is technical in nature and therefore not appropriate for execution on a multilateral venue is removed from the picture,” wrote Howson. “The Esma consultation is unhelpful in the way that it presents non pre-trade transparent trading as including all systematic internaliser and over-the-counter activity, as well as all activity undertaken under a waiver.”

Cboe Europe President David Howson shares his thoughts on recent market performance, Cboe’s response to ESMA on its MiFID II/MiFIR report, and more. Visit the Cboe blog for details – https://t.co/ml70qVwFJQ pic.twitter.com/iRnYCT8fIC

— Cboe (@CBOE) April 24, 2020

Howson also stated that the double volume cap regime should be completely removed, rather than arbitrary alterations made to the current thresholds. MiFID II introduced caps on trading in dark pools with the aim of shifting volumes onto lit markets

“The DVCs have introduced cost and complexity and delivered no clear benefit to execution performance and end investors,” he added.

He continued that there is also no evidence of investor detriment from periodic auctions. “The platforms, including the enhancements Esma proposed last year, have proven themselves as low impact, price-forming mechanisms that deliver beneficial execution outcomes,” said Howson.

However Cboe did express concern that the significant increase in closing auction volume poses a systemic risk to the efficient and orderly running of markets and should be closely monitored by regulators.

“This trend would be further exacerbated if the choice of low impact trading mechanisms, such as those utilising the reference price waiver and negotiated trade waiver is forcefully reduced,” said the letter.